There are many risks associated with investing, but there’s one retirement risk that gets very little attention: Sequencing of returns risk. But what exactly is it and what impact does it have?

The sequence of returns risk involves a complex interplay of market returns, time, and cash inflows and outflows. When investing over a long period, it’s easy to get caught up in short-term market fluctuations. Despite the roller coaster of returns each year, history tells us that over the long term, what really affects results is the long-term average.

If you’re investing a capital base and not making any deposits or withdrawals, the total return you earn will be the same irrespective of the specific order of returns year to year. Conversely, if you are making withdrawals or deposits, the timing of those sales or purchases can become detrimental to returns.

For those in the retirement drawdown phase, your portfolio value is reflective of the market performance and your cash outflows. In the event of a market downturn, those withdrawing can be hit with reduced market rates along with the drawdown on capital.

In this blog, I provide some clarity on how the sequencing of returns affects your portfolio value and some guidelines on how to mitigate sequence risk when withdrawing from a portfolio.

A practical example is the best way to illustrate how this works. If you start with a portfolio value of $100,000 and withdraw $10,000 per year and the total return is 10% one year, 10% the next, and negative 10% in the third year, you’d end up with $80,000 by the end of the third year.

Alternatively, if this return occurred in the reverse order, you’d end with just $75,800 as illustrated below.

This represents how important timing can be during the first few years before and after retirement. It also illustrates that you do not want to be a forced seller in a down market.

From 1900 to 2018, the Australian share market has returned an average of 13.1% per annum. Of those 119 years, there have been 23 negative years (19%), and 96 positive years (81%).

Of the negative years, there are only a handful of years that had consecutive negative years; 1915-16, 1929-30, 1951-52, 1973-74, and 1981-82.

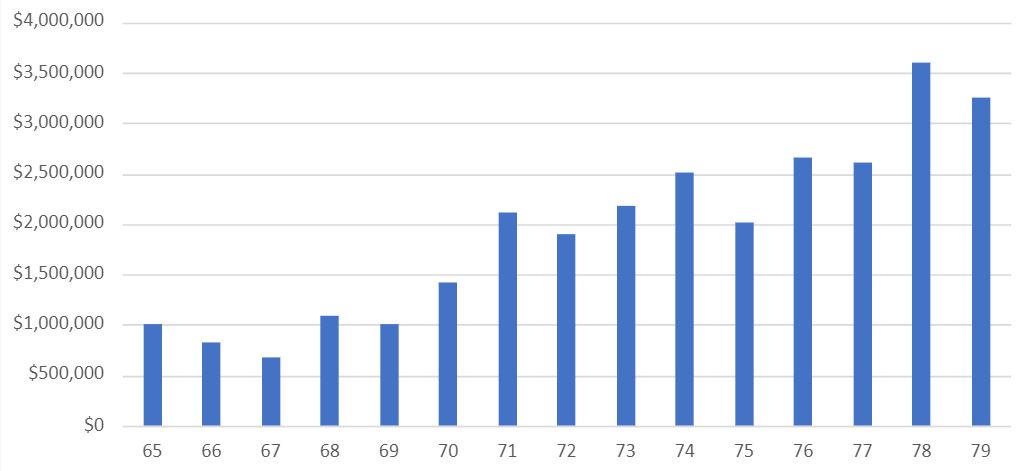

It’s worth understanding the potential risk for investors heading into retirement. I have put together a graph that reflects someone who commenced retirement in 1981, the last time there was consecutive negative return years, with an all-equity portfolio. The example below assumes the investor retiring is age 65 with a portfolio balance of $1,000,000. The investor is withdrawing $40,000 per annum (increasing by 3% each year to keep up with inflation) and the returns mirror the All Ordinaries Accumulation Index (XAOA) starting in 1981. Under this scenario, the portfolio’s value would have decreased in value to $674,291 by the end of the second year due to back-to-back years of negative return and capital drawdown. As a result, the portfolio does not benefit as much when the market rebounds due to the smaller capital base.

Calculation note; Portfolio values are based on a $1,000,000 starting balance with $40,000 annual withdrawals increasing by 3% per year. The returns mirror the All Ordinaries Accumulation Index (XAOA) starting in 1981.

As you can see, the portfolio does recover over the 14-year period reaching $3.24 million by age 79.

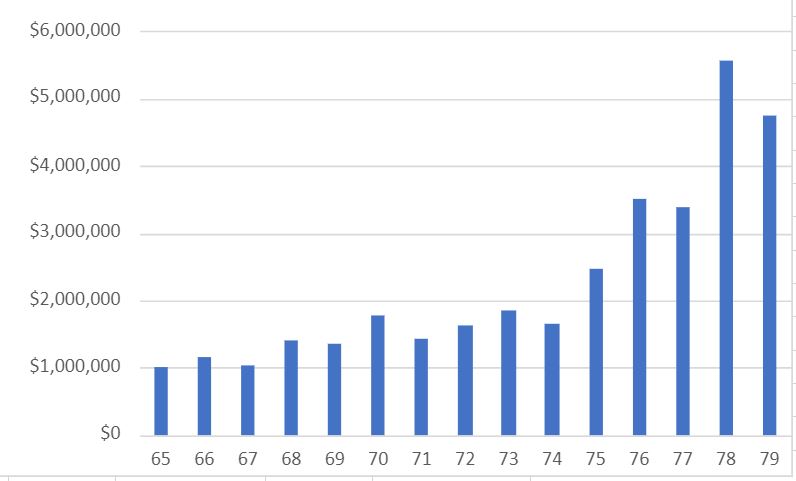

If the sequence of returns was reversed, the outcome would be far superior. The below graph shows the portfolio’s value over the 14-year period which the All Ordinaries Accumulation Index earned the same return as it did from 1981 to 1995, but in the reverse order. By age 79, the portfolio would have reached $4.73 million, almost a $1.5 million difference for the example above. This leaves significant capacity for increasing withdrawal rate, gifting to children and grandchildren, covering the cost for long-term care, or leaving behind a significant inheritance.

The above is an exaggerated example, few retirees come into retirement with an all-equity portfolio. Having an allocation to other asset classes, like fixed income is one of the best ways to mitigate the sequence of returns risk. Although fixed income securities still carry risk from return patterns over time, the range at which they fluctuate is typically smaller and can reduce some of the risks of an equity market downturn. In addition, some investors mitigate this risk by holding surplus cash to fund planned withdrawals for at least one or two years, so they do not have to be forced to sell assets during a market downturn. Although, holding cash in the current interest rate environment may cause other issues.

At Hewison Private Wealth, we manage the sequence of return risks for those in the drawdown phase through multiple strategies. Primarily, we invest across different asset classes that are underpinned by income, for example, fixed income and property. This not only reduces the volatility of the portfolio value and smooth returns over the longer term, but it also provides a steady and reliable income stream that can fund your retirement lifestyle.

In an ideal scenario, we establish a portfolio that generates 4-5% income per annum that can fund your living expenses, whereby you don’t have to sell assets whether a market downturn occurs or not. This way, the capital is preserved, and it can grow into perpetuity.

Another strategy to reduce sequencing return is rebalancing back to the target asset allocation. This is a core philosophy at Hewison Private Wealth and becomes paramount during a market downturn. Using last year as an example, the market downturn caused by the COVID-19 pandemic had the Australian equity market fall by over 30% within a month. During this period, most portfolios became ‘underweight’ equities which signal us to buy additional equities. As the COVID-19 downturn was one of the most severe in recent history, it also proved to be one of the shortest-lived. Rebalancing through the downturn resulted in us buying assets at low prices and capitalising on the upside which reduces the sequencing risk as the portfolio value rebounds quicker.

The sequence of returns risk gets little attention when discussing investing. Understanding how it works and implementing prudent portfolio management can assist in preventing the potential downside, and that’s where our value at Hewison Private Wealth lies.

Hewison Private Wealth is a Melbourne based independent financial planning firm. Our financial advisers are highly qualified wealth managers and specialise in self managed super funds (SMSF), financial planning, retirement planning advice and investment portfolio management. If you would like to speak to a financial adviser on how you can secure your financial future please contact us 03 8548 4800, email info@hewison.com.au or visit www.hewison.com.auPlease note: The advice provided above is general information only and individuals should seek specialised advice from a qualified financial advisor. The views in this blog are those of the individual and may not represent the general opinion of the firm. Please contact Hewison Private Wealth for more information.